.svg)

Joke of the day: What does a spy do when it’s raining? He goes undercover.

News Highlights

Here are some of the market highlights from this week:

- Despite it being a Canadian holiday, the markets took no time off in beating crude prices down. As equities continue to crack, WTI plummeted down to sub-$72/bbl levels, though it recovered slightly to settle at $72.94/bbl, culminating in a fifty-eight-cent loss on the day. As far as geopolitical risk goes, the Iranians seem to be vying for a de-escalation of the current conflict with Israel while simultaneously retaliating against Israel’s recent airstrikes—talk about mixed signals. Abroad, Libya’s largest crude oil field, El Sharara, has been taken offline as a result of an ongoing labour dispute in the country. This means that Libya’s crude output has dropped by ~270 Mb/d overnight, and as of now, it’s unknown how long the outage will last. Over the weekend, China rolled out plans to spur domestic consumer spending as weak domestic demand continues to weigh on growth. As the world’s biggest crude customer, the wider trends of the Chinese economy suggest a concerning state of affairs, as energy figures out of the country have been disappointing to say the least in recent memory. In fact, China’s crude oil imports have fallen to their lowest level since September 2022, with low domestic fuel demand and poor refinery margins leading to a slowdown in refinery runs. We’re still on the bearish side of the fence, and this morning, WTI is trading at $74.735/bbl.

- As much as we would like the figures to break away from the status quo, it seems that natural gas prices are stuck in their ways. On Monday, we saw gas prices give up another two and a half cents to settle at $1.942/MMBtu. Many eyes have been on Hurricane Debby for its potential to disrupt oil and gas infrastructure, though upon touching down on land as a mild category 1 hurricane, there appears to be little if any disruption to the energy sector as it moves up along the east coast. Following three days of storage draws, the United States has returned to injections as temperatures modulate and the need for intensive cooling diminishes. Likewise, the outlook in the east illustrates temperatures easing in tandem for the coming weeks, meaning injections are back and are likely here to stay for the remainder of the season. We’re feeling bearish on the gas front, and this morning, natural gas is trading at $2.085/MMBtu.

- Ameliorating traffic conditions at the Panama Canal will most likely keep very large gas carrier (VLGC) rates lower in the second half of 2024. In fact, the Panama Canal Authority (PCA) has added an additional Neopanamax crossing slot beginning in January 2025 this past week, adding yet another item to the list of signs of easing congestion. For reference, daily Neopanamax auctioned slots will increase to ten in January, which is double the amount advertised for January 2024. Water levels at Gatun Lake, which supplies water to the Panama Canal locks, have been on the rise, and rather quickly, due to the La Niña weather pattern bringing rain by the bucketload since May. Water levels just exceeded eighty-five feet for the first time since March 2023, and going forward, it’s probable that water levels will follow a pattern like what was seen in 2016 and 2020 when La Niña replaced El Niño and brought forth a surplus of rainwater. Good to hear, as the Canal is the shortest avenue from the Gulf Coast to East Asia and is the preferred route for LPG traders, especially in backwardated markets. This morning, Belvieu propane is trading at $0.76000/usg, while Conway is at $0.74125/usg.

- Normal butane prices trended lower this week alongside LST, and the C4/C3 had something of a rally into the end of July before selling off at the advent of August. Isobutane prices felt the same downward pressure, falling off somewhat at the beginning of the month. This morning, Belvieu NTET butane is trading at $0.93875/usg. The Cal 24 strip is sitting at $0.94300/usg. The relative value of butane to crude is 51.63%

Striemer, K. (August 7, 2024). Energy and FX Commentary. National Bank of Canada: Financial Markets.

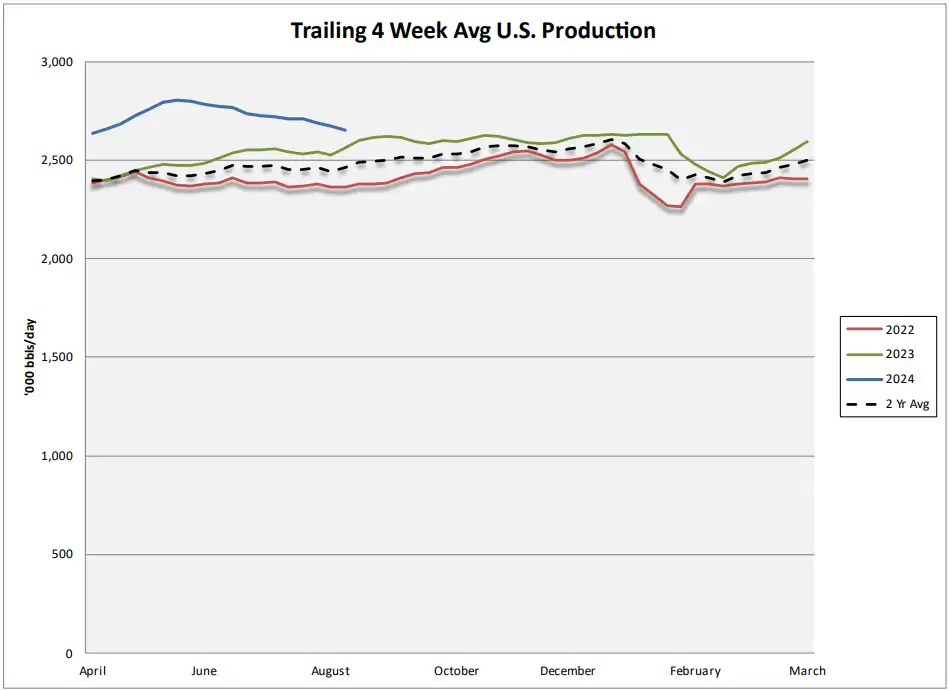

EIA Inventory Stats

Weather Forecast

Price Curves

Contact Information

Please keep Kiros Energy Marketing in mind for your spot or term propane supply requirements. We can offer a variety of price structures (both fixed and indexed) for both the short and long term (‘24/’25, ‘25/’26 and ‘26/’27) contract years at the following lift points:

Northeast lifting locations:

- Albany, NY

- Auburn, ME

- Bellows Falls, VT

- Selkirk, NY

- Oneonta, NY

- Watkins Glen, NY

Michigan Lifting Locations:

- Marysville, MI

- St. Clair, MI

- Bay City, MI

- Grand Rapids, MI

- Gaylord, MI

Mid Atlantic Lifting Locations:

- Stephen’s City, VA

- Branchville, VA

- Baltimore, MD

- Lancaster, PA

- Marcus Hook, PA

- Repauno, NJ (Gibbstown)

- Greensburg, PA

- Dubois, PA

Southeast Lifting Locations:

- Heath Springs, SC

- Hattiesburg, MS

- Dixie Terminals

- Tallahatchie, MS

Marketers:

- Al Lajoie | 403-477-2995 | alajoie@kirosenergy.com

- Sumeet Paul | 403-585-6270 | spaul@kirosenergy.com (Michigan)

- Jeff Steppat | 605-760-0839 | jsteppat@kirosenergyusa.com (Northeast)

- Chris Roth | 913-486-6055 | croth@kirosenergyusa.com

- Pete Kowalewich | 816-547-6870 | pkowalewich@kirosenergyusa.com

Inventory Charts

*Disclaimer: This material is provided for informational purposes only and is not intended as an offer to sell, or the solicitation of an offer to purchase, any commodity. This material contains information that is subject to change and is not intended to be complete or to constitute all the information necessary to evaluate adequately the consequences of buying or selling any commodities.